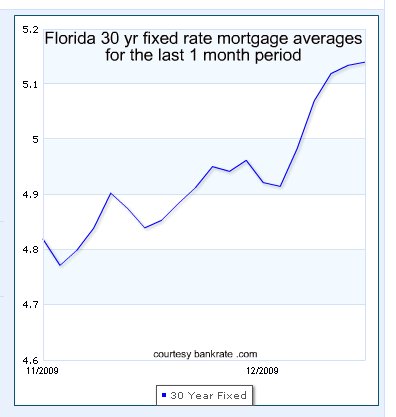

I hope all had a happy, safe time last week and are resting for this week's continuing festivities and the end to a very interesting and challenging year. After a year of crazy low mortgage rates, expect the line on the graph above to continue upward through 2010 if Freddie Mac is right. The mortgage financier expects rates to climb to 6% by the end of 2010.

Our inventory numbers for Monday the 28th of December, 2009 are:

MLS-listed Properties in Cocoa Beach and Cape Canaveral

Condominiums, all prices______567

_____Sold and closed in 2009__402

Single family homes, all prices__120

_____Sold and closed in 2009____77

Condos over $500,000________69

_____Sold and closed in 2009__29

Homes over $500,000_________46

_____Sold and closed in 2009____5

I will post a full year end review the first week of the new year after the listing agents have (hopefully) had time to update their listings. It is apparent now that we will finish 2009 with sales slightly ahead of the last two years.

A little commentary on the numbers so far; all of the sold over-$500,000 homes were in Cocoa Beach, none in Cape Canaveral. Of the 29 sold condos over $500,000, 15 were at the Meridian of Cocoa Beach and only one of the 29 was outside Cocoa Beach, an oceanfront Shorewood unit in Cape Canaveral. Over three quarters of all sold condos in the two cities in 2009 closed for less than $300,000 and just less than two thirds of the sold homes fell in that price range. Expect that trend to continue in 2010.

"You can clutch the past so tightly to your chest that it leaves your arms too full to embrace the present."____Jan Glidewell

.png)

{kind=link}